A question that is popping up a lot more often now from buyers is “How soon can I purchase again after a Short Sale, Foreclosure or Bankruptcy”. As the housing crash started back in 2007, you will start to find that more and more buyers who suffered a financial hardship in the last 3-5 years, will be in a position to qualify to purchase again soon! Here is a cheat sheet that you can use that will help you answer correctly the next time a buyer asks you how soon can they purchase again after suffering either a Short Sale, Foreclosure or Bankruptcy.

Fannie, FHA and VA now fund over 90% of mortgages

Buyers essentially have 3 choices these days when it comes to obtaining financing, as more than 9 out of 10 mortgages are either funded by Fannie Mae/Freddie Mac, the FHA or VA! So if a buyer is looking to purchase and needs financing, it is more than likely they will be using one of these 3.

Therefore if you know the repurchase rules that these 3 entities have in regards to when a buyer can repurchase again after suffering a short sale, foreclosure or bankruptcy, you will now be able to let your clients know exactly when they can purchase again! This will also help you focus your time and efforts accordingly too, for example, if you know someone who is 1 month away from being able to repurchase as opposed to 1 year, you will be able to focus more attention on the buyer who can purchase the earliest!

How soon can I purchase again after a Short sale?

Here are the time lines for when a buyer can purchase again after suffering a Short Sale and they are trying to obtain either Conventional, FHA or VA financing.

Conventional . It is 4 years for Conventional financing, some lenders may allow a 2 year period with compensating variables (for example if they never had a late payment before they short sold)

FHA. It is 3 years for FHA

VA. It is 2 years for VA

How soon can I purchase again after a Foreclosure?

Here are the time lines for when a buyer can purchase again after suffering a Foreclosure and they are trying to obtain either Conventional, FHA or VA financing.

Conventional . It is 7 years for Conventional financing.

FHA. It is 3 years for FHA

VA. It is 2 years for VA

How soon can I purchase again after a Bankruptcy?

Here are the time lines for when a buyer can purchase again after suffering a Bankruptcy and they are trying to obtain either Conventional, FHA or VA financing.

Conventional . For a chapter 7 Bankruptcy it is 4 years and 2 years for a chapter 13 bankruptcy for Conventional financing.

FHA. For a chapter 7 Bankruptcy it is 2 years and 1 year fora chapter 13 for FHA financing.

VA. For a chapter 7 Bankruptcy it is 2 years, and 1 year for a chapter 13 bankruptcy for VA financing.

Reach out to all past clients, friends and family

As the housing crash is now in its 5th year, you will start to find that more and more buyers you talk to who did suffer a financial hardship in the past, will be getting closer to being able to qualify to purchase again. For example, as the VA only needs 2 years from a short sale or a foreclosure, and the FHA only 3 years, you may find some past clients who have already gone past these dates!

Check the dates with any clients you helped short sale in the past, and family or friends you know who also suffered a short sale, and verify how much time has elapsed since their financial hardship, so you can let them know how soon they can re-purchase again. Do the same with past clients, friends and family who suffered a Foreclosure or Bankruptcy too, and verify the dates they suffered their financial hardship and let them know how soon they can purchase again based on these time lines above too.

Help Buyers rebuild their credit now

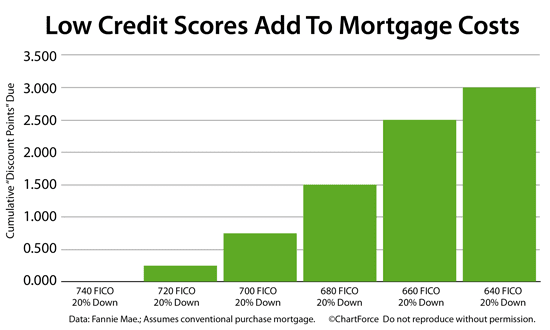

It is also important to find out if your buyer has re-established their credit again since their hardship, because even though the required time line of say 2 or 3 years may have passed for FHA financing, it is important they have started to rebuild their credit and have the required fico scores needed too. Fyi FHA and the VA only require a 620 credit score to repurchase again.

Give them tips on how to rebuild their credit again, so they can get in a position to repurchase asap! The first step is for someone to get a copy of their credit report to verify if their financial hardship or discharge is reporting correctly and to also see what their scores are. Let your buyers know they can go to www.annualcreditreport.com to get a FREE copy of their credit report (they are allowed 1 free per year). The next step is to start rebuilding their scores, here are 5 Quick Credit Tips that you can share that will help someone build their credit faster.

Tomorrows Buyers

Tomorrows buyers are the people who suffered a financial hardship in the recent past! Many of these people I talk too assume it takes anywhere from 4-7 years before they can purchase again, and a lot of them are genuinely shocked when they realize that the FHA for example allows them to purchase again after just 2-3 years!

Start educating people now via email campaigns or facebook posts, letting all your clients, friends and family know about these time lines above in case they are unaware of the time frames necessary before they can re-purchase again. Let them know how important it is that they rebuild their credit too, and if they need credit tips on how to rebuild their credit they should contact you.

I hope you found this information useful. If you have any questions in regards to these programs or time lines listed above, please feel free to contact me directly at 858-200-9602 or via email at mdeery@citywidefinancialcorp.com . I look forward to chatting soon.