During 2018 40% of all home buyers were first time buyers, this number is expected to increase in 2019. Over 80% of these first time buyers use low down payment programs to purchase a home. A newly released report by Apartment List advised that saving for a down payment is the primary financial obstacle keeping millennial renters from purchasing homes, with 61.7% of respondents who plan to buy saying that they can’t afford a down payment. Not enough first time or millennial buyers know about the different low down payment options available to help them buy a home. I summarized below the Top 4 purchase programs available for first time buyers.

Understanding First Time Buyers and Millennial Buyers

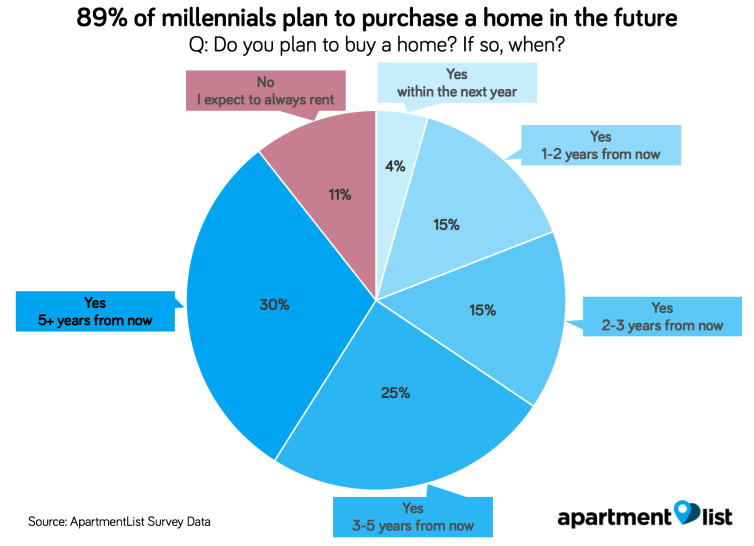

A newly-released report from Apartment List analyzed data from 6,400 surveyed millennials on their plans for home ownership.

With Millennial’s on the verge of surpassing Baby Boomers as the nation’s largest generation, the question of when and if they will purchase homes looms large over the housing market.

While the overwhelming majority of those surveyed would like to purchase a home at some point in the future, far fewer are financially prepared to do so in the near term.

Key findings include:

89.4% of millennial renters say that they plan to purchase a home at some point in the future, but just 4.4% expect to do so within the next year, while 30.4% percent say that they won’t buy for at least five years.

Of those millennial renters who plan to purchase a home, 48% have zero down payment savings, while just 11% have saved $10,000 or more.

Specifically, we find that saving a down payment is the primary financial obstacle keeping millennial renters from purchasing homes, with 61.7% of respondents who plan to buy saying that they can’t afford a down payment.

Too many Millennial and First Time buyers don’t know about the different low down payment programs available to help them buy a home, or programs that will cover ALL of their down payment and ALL of their closing costs.

Here is a summary of the best 4 purchase programs available for first time buyers.

1. Buy a Home up to $500,000 with Only 3% Down Conventional Financing and No Monthly PMI.

With the new higher conventional loan limit of $484,000 available for buyers in California, a first time buyer can now purchase a home up to $500,000 with only 3% down conventional financing.

Buyers also have the option to eliminate the monthly mortgage insurance “PMI” from their monthly mortgage payment.

All of the down payment can be gifted too, so this is a great option for buyers to purchase right away if they do not have the down payment saved up yet.

Co-signers are allowed to help buyers qualify for a home purchase.

Only a 620 credit score is required to qualify for conventional financing.

Click HERE for more information on how to qualify for Freddie Mac’s New conventional 3% down HomeOne program with No PMI, there is a Q&A section included too.

2. Buy a Home up to $765,000 with Only 5% Down Conventional Jumbo Financing with No Monthly PMI.

If a first time buyer needs to finance a mortgage over the conventional loan limti of $484,350, they are eligible to use conventional jumbo financing up to a maximum loan amount of $726,525. This means a buyer can now purchase a home up to $765k with only 5% down.

Buyers also have the option to eliminate the monthly mortgage insurance “PMI” from their monthly mortgage payment.

Buyers in San Diego County can purchase a home up to $725,000 with only 5% down and No PMI.

Buyers in LA County, Orange County and SF County for example, can purchase a home up to $765,000 with only 5% down and No PMI.

All of the down payment can be gifted too, so this is a great option for buyers to purchase right away if they do not have the down payment saved up yet.

Only a 620 credit score is required to qualify for conventional jumbo financing.

Co-signers are allowed to help buyers qualify for a home purchase.

Click HERE for more information on how to qualify for the conventional Jumbo 5% down program with No PMI, there is a Q&A section included too.

![]()

3. Buy a Home up to $750,000 with only 3.5% Down FHA financing

FHA financing is a very popular program with first time homebuyers. With it’s easier qualification rules for buyers with less than perfect credit, the FHA helps many first time buyers finance a home that would not be able to otherwise.

The minimum down payment with FHA financing is only 3.5%. The FHA increased their CA conforming loan limit recently from $453,100 to $484,350, so this means a buyer can purchase a home up to $500,000 with only 3.5%.

In higher cost markets like LA, Orange Co and SF etc, a FHA buyer can purchase a home up to $750,000 with only 3.5% with a FHA jumbo loan.

In San Diego county, a buyer in San Diego can purchase a home up to $715,000 with only 3.5% down.

In Riverside and San Bernardino counties, a buyer can purchase a home up to $500,000 with only 3.5% down.

Only a 580 credit score is required to qualify for 3.5% down FHA financing.

Co-signers are allowed to help buyers qualify for a home purchase.

4. Zero Down Payment and Closing Cost Assistance For Buyers

If a buyer would like ALL of their down payment and closing costs covered to purchase a home, we have a terrific program available for buyers that combines a Conventional and CalHFA loan or a FHA and CalHFA loan.

Buyers can purchase a home up to $700k in certain counties with No down payment and No closing costs.

CalHFA (California Housing Finance Agency) offers down payment and closing cost assistance loan programs to help first time buyers purchase a home. A first time buyer is defined as someone who has not owned a home in 3 years.

This program is available with both conventional and FHA financing. CalHFA gives buyers a small 2nd mortgage up to 3.5% to help cover the minimum down payment due with conventional and FHA financing.

If buyers don’t have enough funds for their closing costs, CalHFA will give buyers an additional small 3rd mortgage of up to 4% to help cover ALL their closing costs. Many buyers using this program only have to pay the upfront appraisal fee out of pocket.

Payments on the CalHFA 2nd or 3rd mortgage loans are deferred for the life of the first mortgage. The terms are the same as the first mortgage. There are no payments due unless you sell or refinance.

Click HERE for more information on this program and examples of how you can purchase a $450k or $550k home with zero down payment and No closing costs.

If you have questions about any loan program or you would like to get approved for one of these options above, please call me at 858-442-2686.

I look forward to chatting soon.