VA Purchase Tips for Home Buyers and Real Estate Agents!

VA financing is one of the best mortgage products available in the market today for home buyers, as the VA makes it easy for their members to purchase a home with zero down financing. This list of VA frequently asked questions and VA tips will help you understand the in-and-outs of how the VA mortgage program works. I also included 6 tips below too that you can use to help get a VA purchase offer accepted.

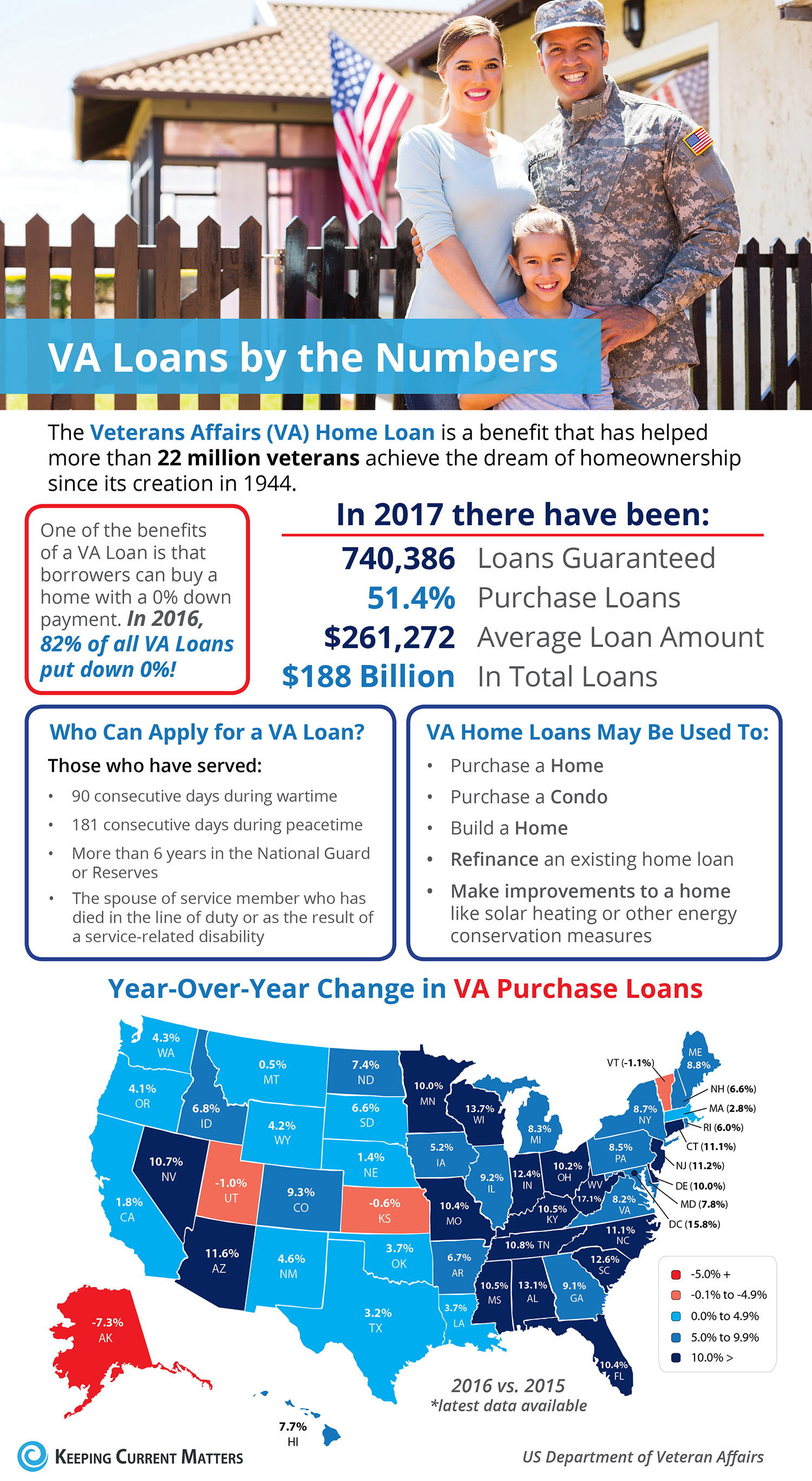

VA Loans by the Numbers

in 2017, 82% of all VA loans put down 0%. Here is a snapshot of who can apply for a VA loan and what type of VA financing is available.

Who is Eligible for VA financing?

A veteran is eligible for VA financing if he/she served on active duty in the Army, Navy, Air Force, Marine Corps, or Coast Guard and was honorably discharged after 24 continuous months of active duty, or the full period for which called, or ordered to active duty, but not less than 90 days (during wartime) or 181 continuous days (during peacetime).

How Much Home Can I purchase With a Zero Down VA Mortgage?

VA buyers qualify for zero down financing up to their county loan limit. For example, a VA buyer can get zero down financing in San Diego up to $612,950, $636,150 in LA county and Orange County, and $424,100 for Riverside county. You can check your county loan limit HERE .

There is only a small down payment due if a buyer needs to purchase over the county limit. On a $700k purchase in San Diego for example, the down payment due is only $21,762.

We can also give a VA buyer a 3% lender credit to cover ALL their closing costs. This means a VA buyer can purchase a home with No down payment due or closing costs either, and this also includes a credit for the appraisal fee.

What is the Minimum Credit Score to Qualify For VA Financing?

Most VA lenders require a 620 credit score to offer zero down VA financing. We have a couple of lenders who only require a 580 score to qualify for zero down financing.

Do VA Buyers Pay Any Monthly Mortgage Insurance?

VA buyers do not need to pay any monthly mortgage insurance (MI) on their loans even up to 100% of the property value, as VA loans are backed by the government.

Can VA Buyers Purchase a 2-4 Unit Property?

The VA allows their military buyers to purchase a 2-4 unit home with zero down VA financing. VA financing is for owner occupied financing, so the VA borrower would live in one unit and rent out the other 1-3 units.

You can also use the rental income from the other 1-3 units to qualify for a loan. This is a great way for VA homebuyers to start out as a real estate investor.

- You can finance up to a loan amount of $784,700 on a 2 unit property.

- You can finance up to a loan amount of $948,500 on a 3 unit property.

- You can finance up to a loan amount of $1,178,750 on a 4 unit property.

How are VA interest Rates Compared to Other Loan Programs?

VA mortgage rates are the lowest in the industry and are typically .375% lower than conventional rates.

What is the VA Mortgage Waiting Period after a Foreclosure, Short sale or Bankruptcy?

Short Sale: It is only 2 years before a buyer can repurchase again using VA financing.

Foreclosure: It is only 2 years before a buyer can repurchase again using VA financing.

Bankruptcy: For a chapter 7 Bankruptcy it is 2 years and 1 year for a chapter 13, before a buyer can repurchase again using VA financing.

Tips for VA Buyers and Sellers – The Misconception Sellers Have About VA Closing Costs

There is a misconception out there that the seller must pay for some or all of a VA buyer’s closing costs. The seller is NOT required to pay ANY costs for the buyer, but is allowed to pay up to 4% for VA loans.

But there are certain “VA non-allowable” costs for which a VA buyer is forbidden to pay, (for example No escrow fees, wiring, notary, tax service or processing fees etc are allowed to be charged).

Here is a good tip to help get a VA offer accepted, so this issue of who covers these VA non allowable fees does not become an issue. Write the following verbiage in the purchase contract, so the seller is not put off by the VA offer: “Seller not responsible for any buyer closing costs, regardless of the selected loan program. All agency-related “non-allowable” costs to be borne/paid by lender”.

This means the VA Non-Allowable fees will be paid by a lender credit instead of the seller, we do this for all our VA buyers.

So now the seller will NOT dismiss the VA offer right away, does NOT have to cover any closing costs, negotiations are easier, and the buyer and seller can strike a deal.

6 Tips to Help Get Your VA Purchase Offer Accepted

Sometimes I hear from buyers and agents that it is tougher to get a VA purchase offer accepted. It is true that some sellers will look the other way when they see a VA purchase offer, due to the zero down payment “no skin in the game”, and the assumption they will also need to cover the VA closing costs. Here are 6 tips to help your VA purchase offer get accepted

1. Include a personal cover letter with your purchase offer

A good idea in this competitive housing market is for the buyers to write a personal cover letter to the seller. Include this letter with your offer that introduces the family and why they are the right candidate to purchase the home. Include a family picture too.

If you can tug at the heart strings of the seller, they may be more inclined to choose your offer over others. There are plenty of sellers who will be happy to sell their home to a military family to thank them for their service. Many agents and buyers tell me this strategy works!

2. Include a VA DU underwriting approval with your offer

Include a VA DU underwriting approval with your offer. A DU (desktop) underwriting approval is when a buyer’s loan application and credit report has been ran through the VA’s automated underwriting systems and was approved.

A DU underwriting approval displays the most important information on a buyer’s profile, which gives the seller a better idea of the strength of the buyer. For example, a DU approval displays a buyer’s credit scores, debt to income ratios, assets, reserves, any applicable down payment and the type of loan program they are approved for.

3. Provide proof of reserves/assets/down payment funds to strengthen offer

The zero down payment requirement with VA means less skin in the game. We can’t argue with this because VA allows 100% financing, so this does amount to very “little skin in the game” from a buyer.

Therefore it’s a good idea to include proof of reserves and assets and any applicable down payment funds along with your offer, so this shows the seller the buyer has applicable funds to close if any additional funds are needed to close the transaction.

4. Increase your deposit

Want to show a seller how serious your offer is? Consider putting down a bigger deposit in earnest money. This may seem risky for some, but earnest money is there for a reason. If you are uncertain about putting a “noticeable” amount of earnest money on the table, it may be a sign to the seller that you are uncertain about the house itself.

Assuming you hold up your end of the bargain and you have the right contingencies in place, it won’t cost you any more in the long run since the deposit goes towards your down payment if financing is involved.

*As a VA buyer typically qualifies for zero down financing, they will get their deposit back at closing

5. Be flexible and don’t ask for any seller credits

It’s a good idea to ask the seller’s agent upfront what you can do to make the offer more enticing to the sellers.

For example, can you be flexible on the closing date for the seller?

Also, a purchase offer asking for seller credits to pay for your closing costs will usually place behind an offer that does NOT ask for any seller credits.

SOLUTION: To make a buyers offer more competitive, the lender can pay for some or ALL the buyers closing costs with a lender credit.

How does this work? Instead of taking say a 4% 30 year fixed rate, take a higher rate of 4.25% instead, and now there is a lender credit of roughly 2% available that can be used to pay towards a buyers closing costs.

Not only is this a good negotiating tactic so the buyer and seller can strike a deal, but of course it saves a buyer money too. We present this option to all our buyers.

Another Tip. In today’s competitive purchase market, another tip is to offer to pay for the sellers Owners title policy and transfer tax. These fees only amount to roughly $2,500 on a $400k home.

6. Close the Transaction Faster

Being able to close a transaction faster is another way to entice the seller to accept your offer in this competitive market.

For example, if a seller is reviewing 3 offers, and there is a 21 day offer, a 30 day and 45 day offer, often the seller will go with the faster closing.

My company Citywide Financial Corp can close a Conventional, FHA or VA Purchase Transaction in 17 – 21 days. We have an outstanding team set up and dedicated to help close transactions fast.

If you have any questions about any of these tips above or getting approved for financing, please do not hesitate to contact me directly at 858-442-2686. I look forward to chatting soon.

P.S. If you would like to be updated faster on important industry news or any new loan programs that come out, please join my Facebook page .

Tags: 100% VA financing, tips to help VA buyers get approved, VA buyers, VA Purchase Tips for Home Buyers and Real Estate Agents, VA zero down financing

This entry was posted on Friday, November 10th, 2017 at 10:54 pm and is filed under VA Purchase Tips for Home Buyers and Real Estate Agents!. You can follow any responses to this entry through the RSS 2.0 feed. Responses are currently closed, but you can trackback from your own site.